“The investor’s chief problem and even his worst enemy is likely to be himself.”

— Benjamin Graham

Quite often, markets remind us that uncertainty is simply part of investing. Our behavior, emotions, and how we react to them matter far more than prediction.

During market volatility, headlines tend to grow louder, and noise floods the news. It’s completely normal to feel uneasy. But, during this time, consider stepping back and taking a look at history. While history won’t necessarily predict what’s to come next, it will help us understand how markets behave over time.

Understanding the difference between a bear market and a bull market and how to respond to each is critical. This may help you protect long-term wealth, generate sustainable retirement income, and avoid costly emotional mistakes.

Key Takeaways:

- Bear markets are temporary. Don’t let emotional decisions become permanent.

- Bull markets may build wealth but require discipline.

- In our view, retirees’ portfolio strategy should include liquidity, rebalancing, and structure, no matter the market.

- A well-built financial plan can help you stay confident in any market cycle.

Bear Market vs. Bull Market

At its core, the difference is straightforward, but the implications for retirement planning are significant.

What is a bear market?

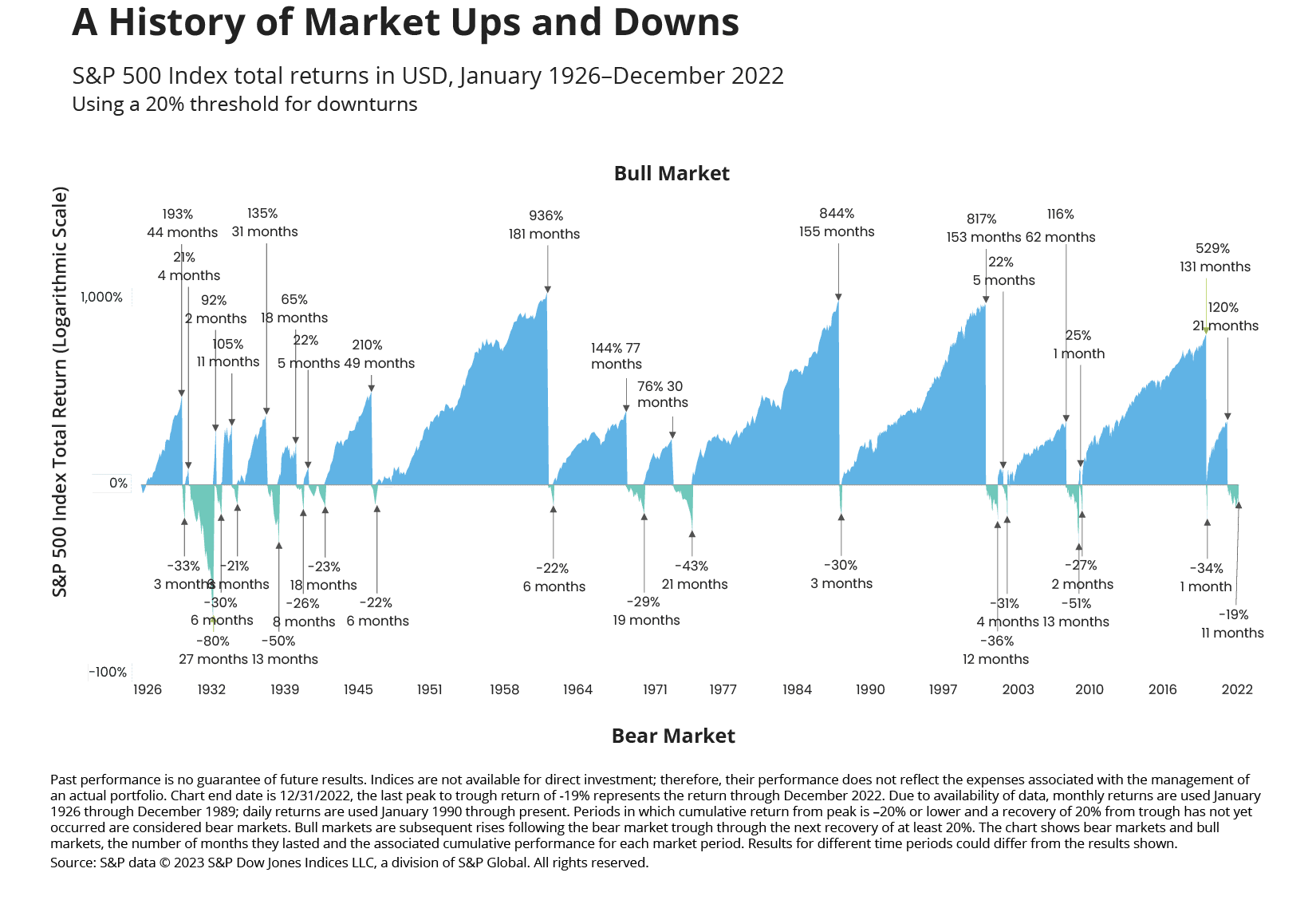

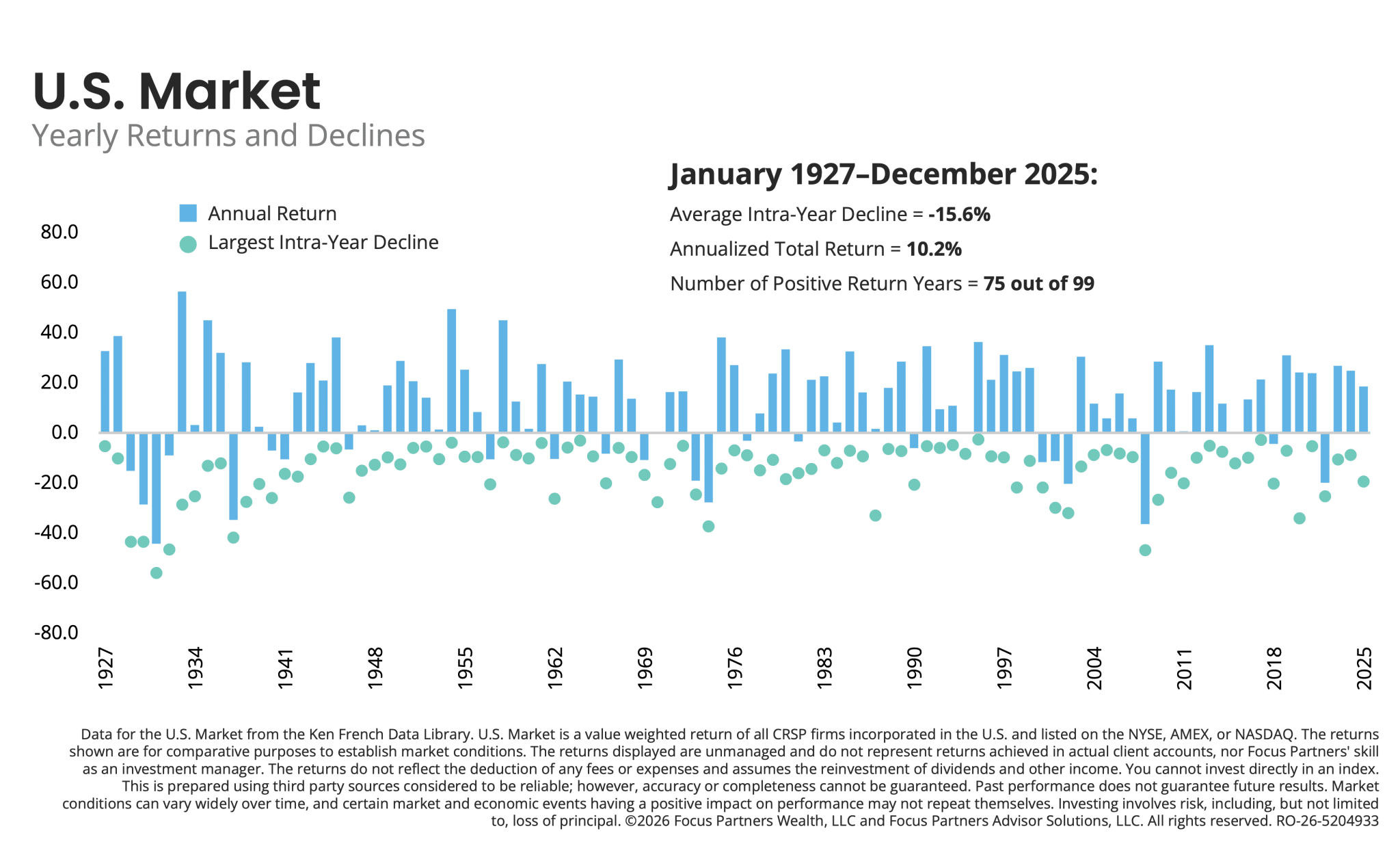

A bear market is typically defined as a decline of 20% or more from a recent market peak to trough. Bear markets never feel comfortable, but they are far from unusual. Over the past 50 years, markets have experienced multiple declines, each unsettling in the moment, yet temporary in nature.

Typical Indicators of a Bear Market

- Sustained market declines over weeks or months

- Negative investor sentiment

- Increased volatility

- Often (but not always) tied to economic slowdowns or recessions

Average Duration of a Bear Market

As you can see, some declines were sharp and short. Others were deeper and lasted longer. Still, bear markets tend to recover faster than bull markets fall. Since 1949, the longest bear market was 1.7 years. During that same period, bear markets averaged 1 year in length and averaged a 31% decline.

The key is to focus on what follows a bear market, not how far the markets may fall during the bear market. As Peter Lynch once famously said, “Far more money has been lost by investors in preparing for corrections, or anticipating corrections, than has been lost in the corrections themselves.”

Bear market recovery timelines tell a much more important story. Even in the most difficult example of the past half-century (the early 2000s decline), the recovery to new highs took roughly five years. That period represents the extreme case. Most recoveries were meaningfully shorter. In March and April 2025, markets technically entered bear territory, yet still finished positive for the year.

History tells us: Markets do fall, sometimes significantly, but they recover. Recovery has been the rule, not the exception.

What is a bull market?

A bull market is the period between bear markets when markets recover and rise 20% or more.

Typical Indicators of a Bull Market

- Sustained upward price movement

- Improving investor confidence

- Expanding economic growth

- Increasing corporate earnings

Average Duration of a Bull Market

Bull markets historically last longer than bear markets. Long-term wealth creation typically occurs during these periods. Since 1949, the longest bull period was 12.3 years. On average, they have lasted 5.3 years with a total return of +254%.

Markets spend a surprising amount of time near all-time highs. Many investors hesitate to invest at highs, assuming a correction must be imminent. However, history shows that investing at market highs has produced outcomes very similar to investing at other times. New highs are often followed by even higher levels over time.

The real risk is rarely investing at highs.

The real risk is stepping away and missing the full cycle of decline, recovery, and growth.

Key Differences and Similarities

| Bear Market | Bull Market |

| 20+% decline from peak | 20+% rise, sustained upward movement |

| Driven by fear and uncertainty | Driven by optimism and growth |

| Volatility increases | Confidence increases |

| Feels uncomfortable | Feels easy |

Bear markets and bull markets are both phases of the same long-term cycle. Over the past 50 years, markets have moved through multiple bears and bulls, yet the long-term trend has been upward. Understanding this context is especially important for retirees. The markets are a perpetual uptrend with temporary declines.

How Retirees Can Respond in a Bear Market

Bear markets never feel comfortable. For those in or nearing retirement, investment decisions are generally guided by strategy, not emotion.

- Protect Liquidity to Support Reliable Cash Flow

A well-constructed portfolio is not only built for growth, but more importantly, for its durability. Well-constructed portfolios are nimble during market declines. In practical terms, this means your portfolio should be structured so that spending needs are not dependent on selling equities during a downturn.

Thoughtful pre-planning includes:

- A disciplined 3-4 year liquidity ladder to support withdrawal needs without sales at unfavorable prices.

- Sufficient fixed income streams and other non-equity assets to provide stability and reliable cash flow.

2. Rebalance Your Portfolio

Market declines generally do not prevent portfolios from growing; they reward disciplined behavior. In simple terms, it is the consistent process of selling high and buying low. Disciplined rebalancing often allows a well-designed plan to remain on course, even during market stress.

Rebalancing includes:

- Trimming areas that have held up relatively well.

- Adding to areas that have declined.

3. Avoid Emotional Decisions

Market volatility has a way of triggering emotional responses. Headlines intensify. Fear rises. The urge to act grows stronger. Yet most long-term investment mistakes are not caused by markets themselves, but by investor reactions to those markets. In many cases, the most effective action is not a dramatic change, but disciplined consistency.

Emotional reactions include:

- Selling after declines, which locks in losses.

- Waiting too long for clarity and missing the recovery.

- Trying too hard to time exits and re-entries.

How Retirees Can Respond in a Bull Market

Bull markets tend to bring a different type of emotion: overconfidence. Again, this too should not dictate strategy. It’s easy to feel tempted to increase risk, especially concentrated risk. Ultimately, stay aligned with long-term goals rather than short-term noise.

- Rebalance Gains

Just as during bear markets, it’s important to remain disciplined during bull markets. Consider trimming your appreciated positions to maintain pre-planned target risk levels.

2. Avoid Overexposure

Keep in mind that a strong stock market should not eliminate your portfolio diversification. In our view, portfolio durability should matter more than maximizing returns for retirees. Keep income planning central to your strategy.

3. Remain Invested and Structured

As mentioned, bull markets tend to last substantially longer than bear markets. However, your portfolio structure should remain relatively the same. Don’t worry about trying to predict the next downturn; maintain a plan that navigates both markets.

Why Financial Planning Matters

For high-net-worth retirees and those nearing retirement, your financial planning goes beyond portfolio returns. It also includes sustainable withdrawal strategies, tax-efficient income distribution, estate and legacy planning, and risk management. A good financial advisor goes a long way to help you remain calm during market turbulence.

Time horizon also matters. Even in retirement, financial plans often extend 5, 10, or even 15+ years. History shows that even prolonged market declines have allowed time for recovery within those horizons. As long as portfolios are structured properly, temporary market stress generally should not necessarily translate into permanent financial impact.

Final Thoughts: Control What You Can Control

“The big money is not in the buying and selling, but in the waiting.”

–Charlie Munger

Markets will continue to move through cycles. There will be periods of optimism and periods of uncertainty. A thoughtful plan, proper portfolio construction, and disciplined execution remain the foundations of long-term planning success.

This communication is for informational purposes only. The content does not purport to present a complete picture, but Focus Partners believes the information is representative of issues and needs facing some clients. This should not be construed as specific investment, tax, or legal advice. Individuals should seek advice from their wealth advisor or other advisors before undertaking actions in response to the matters discussed. No client or prospective should assume the above information serves as the receipt of, or substitute for, personalized individual advice.

This represents the opinions of Focus Partners and presents information that may change due to market conditions or other factors. Nothing contained in this communication may be relied upon as a guarantee, promise, assurance, or representation as to the future. Past performance does not guarantee future results. Market conditions can vary widely over time, and certain market and economic events having a positive impact on performance may not repeat themselves. The charts and accompanying analysis are provided for illustrative purposes only. Investing involves risk, including, but not limited to, loss of principal. Numerous representatives of Focus Partners may provide investment philosophies, strategies, or market opinions that vary. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

This is prepared using third party sources considered to be reliable; however, accuracy or completeness cannot be guaranteed. The information provided will not be updated any time after the date of publication.

Please be advised that Focus Partners only shares video and content through our website or other official sources. Services and investment advice are only provided pursuant to an advisory agreement with the client. Focus Partners’ Form ADV Part 2A and 2B and Privacy Statement will be provided as required by law and include a description of fees payable for investment advisory services.

Services are offered through Focus Partners Advisor Solutions, LLC and Focus Partners Wealth, LLC (collectively referred to in this document as “Focus Partners”), SEC registered investment advisers. Registration with the SEC does not imply a certain level of skill or training and does not imply that the SEC has endorsed or approved the qualifications of the RIAs or their representatives. Prior to January 2025, Focus Partners Advisor Solutions was named Buckingham Strategic Partners, LLC, and Focus Partners Wealth was named The Colony Group, LLC. ©2026 Focus Partners Wealth, LLC and Focus Partners Advisor Solutions, LLC. All rights reserved. RO-26-5246722

Focus Partners Advisor Solutions

When advisors work with Focus Partners Advisor Solutions, they gain the strength of a nationwide community of wealth management professionals. With the support of a diverse team of financial planning leaders, tax professionals, investment researchers and portfolio managers, advisors are able to orchestrate a bespoke plan, tailored to each client’s unique situation. Clients benefit from Focus’s team of dedicated professionals who are constantly exploring and assessing the ever-changing landscape of investments, tax code, markets and planning strategies—with a singular focus on maintaining an evidence-driven, fiduciary approach that puts client’s interests first.